The SaaS Rule of 40 in 2026: What It Hides and Why It's Not Enough

TLDR

- The SaaS Rule of 40 adds your revenue growth rate to your profit margin. A score of 40% or more is considered healthy, but this single number can be deeply misleading.

- Two companies scoring 40 can have opposite futures. A company with 35% growth and 5% margin is compounding value; one with 5% growth and 35% margin is harvesting a stagnant business.

- For early-stage SaaS (sub-$10M ARR), the Rule of 40 is largely irrelevant and penalizes necessary investments in growth. The burn multiple is a far more useful metric at this stage.

- The Rule of X is a successor framework that weights growth 2-3x more heavily than profitability, reflecting how public markets actually value SaaS companies.

- A blended Rule of 40 score hides revenue quality. Decomposing the metric by customer cohort and analyzing Net Revenue Retention (NRR) reveals whether your growth is durable or if you're on an acquisition treadmill.

Consider two SaaS companies. Company A is growing at 35% with a 5% EBITDA margin. Company B is growing at 5% with a 35% EBITDA margin. Both score a perfect 40 on the SaaS Rule of 40.

On paper, they are equals. In reality, they inhabit different universes.

Company A is compounding its way to market leadership. Company B is efficiently harvesting a business that has stalled. Yet the most widely cited metric in SaaS finance treats them as interchangeable. This is the central problem with the Rule of 40: it tells you if you're in the ballpark of healthy performance, but it tells you almost nothing about whether that performance is durable. It treats growth and profitability as equals when one compounds and the other does not.

The Rule of 40 is not a health score; it's a composition problem.

This guide is for operators who know the basic formula but want to understand how the metric is actually used in boardrooms and investor diligence. We'll cover how to calculate it correctly, what the benchmarks look like in 2026, and why the smartest operators are already moving beyond it to frameworks like the Rule of X.

What Is the SaaS Rule of 40?

The SaaS Rule of 40 is a financial benchmark that adds a company's revenue growth rate to its profit margin. If the sum equals or exceeds 40%, the company is considered to be balancing growth and profitability at a healthy, sustainable level for a mature business.

The formula is straightforward:

Revenue Growth Rate (%) + Profit Margin (%) ≥ 40%

The concept was popularized by investor Brad Feld in a 2015 blog post, where he attributed it to an unnamed late-stage investor. Critically, it was originally applied to companies with over $50 million in annual revenue. This is the non-consensus boundary most generic definitions miss: the Rule of 40 was designed as a minimum threshold for mature companies, not a universal health score for a $3M ARR startup.

Despite its narrow origin, its simplicity has made it the default shorthand for SaaS financial health. Yet, achieving it is harder than it looks. According to McKinsey research covering over 200 software companies from 2011 to 2021, only about one-third consistently achieved Rule of 40 performance, and a mere 16% managed to exceed it for the majority of that period.

How to Calculate the Rule of 40 for a SaaS Company

The math is trivial. The challenge—and the source of most misleading scores—is choosing the right inputs. Your Rule of 40 score is only as reliable as the metrics you feed it, and inconsistent choices can paint wildly different pictures of the same business.

Choosing the Right Growth Input: ARR Growth vs. Total Revenue Growth

For a subscription-based SaaS business, year-over-year (YoY) Annual Recurring Revenue (ARR) growth is the correct input. Not total revenue growth.

Total revenue often includes one-time professional services, implementation fees, and other non-recurring charges. These can inflate the growth number without reflecting the health of the core subscription engine. Most serious investors and board decks use ARR growth (or MRR growth for earlier stage companies) precisely because it isolates the predictable, compounding nature of the business model.

The main exception is for usage-based SaaS models, like those of Snowflake or Datadog, where contracted ARR is ambiguous. In these cases, using the annualized revenue run rate from the most recent quarter is the pragmatic and accepted choice. For everyone else, stick to ARR growth.

Choosing the Right Profitability Input: EBITDA, FCF, or Operating Margin?

Adjusted EBITDA margin is the most common profitability input, but it's not the only one, nor always the best. Free Cash Flow (FCF) margin is increasingly preferred by sophisticated investors because it measures actual cash generation, sidestepping accounting adjustments that can obscure a company's true cash position.

Operating margin sits somewhere in between; it captures operating expenses but misses the impact of capital expenditures and changes in working capital.

Here's a practical rule of thumb:

- Use Adjusted EBITDA Margin for internal benchmarking and most board reporting. It's the common language.

- Use FCF Margin when preparing for investor due diligence or fundraising. Growth equity firms like Bessemer and Iconiq will almost certainly recalculate your numbers using FCF margin anyway. Frameworks like the Bessemer Efficiency Score are built on it.

A quick example shows why this matters. A company with 25% YoY ARR growth and an 18% adjusted EBITDA margin scores a 43, passing the test. But if that same company has high capital expenditures or unfavorable working capital changes, its FCF margin might be just 5%. Using that input, its score drops to 30. Same company, different inputs, opposite conclusions.

Why Two Identical Rule of 40 Scores Can Mean Opposite Things

Let's return to our two companies, both scoring a 40.

- Company A: 35% ARR Growth + 5% EBITDA Margin = 40

- Company B: 5% ARR Growth + 35% EBITDA Margin = 40

The Rule of 40 treats these as equivalent outcomes. They are not.

Over three years, Company A's revenue compounds. At a 35% growth rate, its ARR will more than double in under three years. Even with a modest 5% margin, its absolute profit dollars are growing rapidly because the revenue base is expanding. It's building enterprise value.

Company B's revenue, meanwhile, barely moves. At 5% growth, it takes over 14 years to double its ARR. The 35% margin looks healthy, but it's a percentage of a stagnating base. Its absolute profit is capped, and the business is slowly becoming irrelevant. It's liquidating its future for today's margin.

This is the metric's fundamental flaw: growth compounds, and margin on a flat base does not.

Investors know this. It's why public market data from sources like the Bessemer Cloud Index and Meritech Capital consistently shows that revenue growth explains far more of the variance in SaaS valuation multiples than profitability does. A point of growth is simply worth more than a point of margin. If you are optimizing your Rule of 40 score by aggressively cutting costs at the expense of sustainable growth, you are optimizing for the metric while destroying the outcome it was meant to measure.

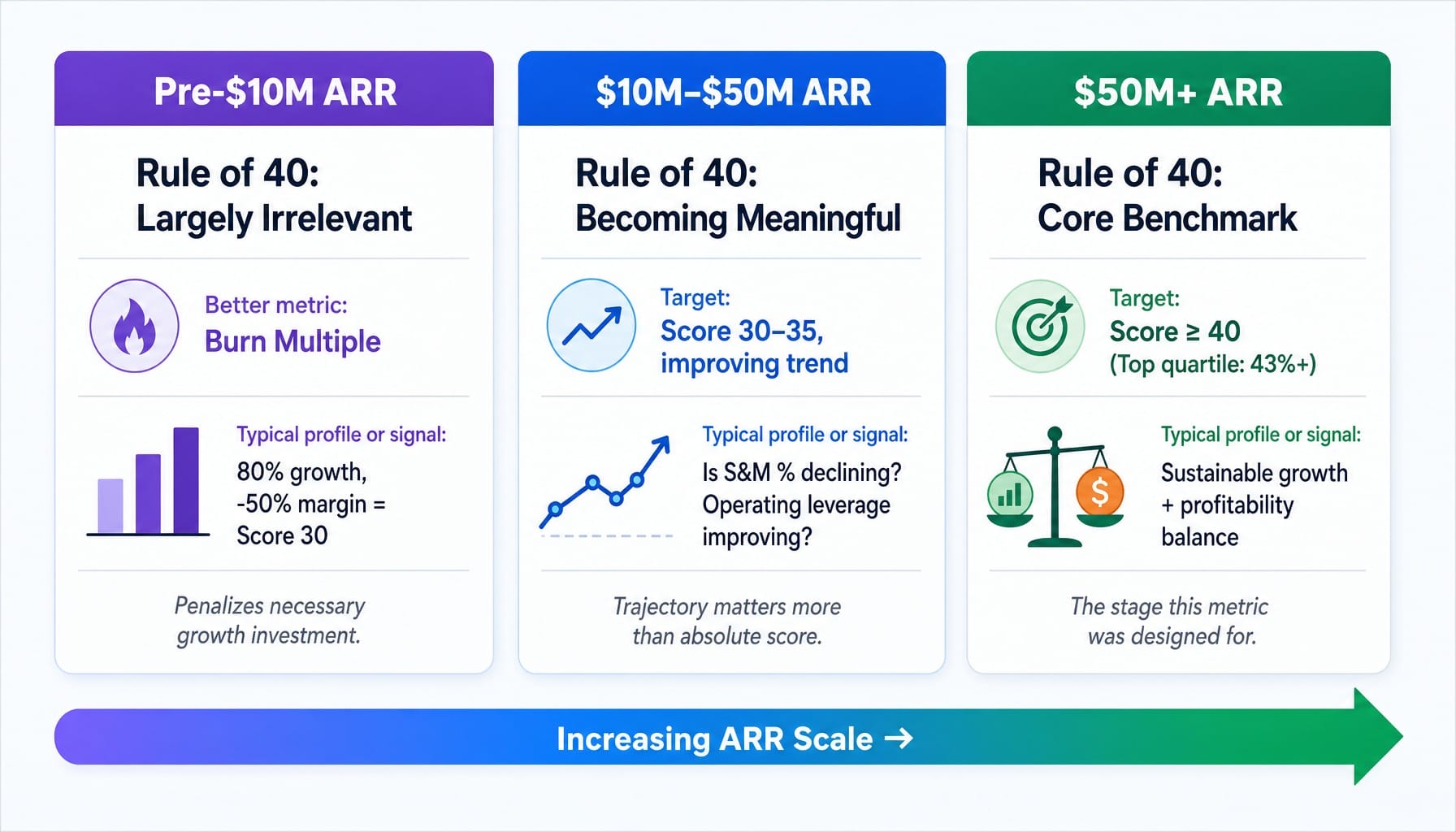

Rule of 40 Benchmarks at Different ARR Stages

The Rule of 40 was designed for companies with over $50M in revenue. Applying it uniformly across all stages is a common but critical error. The target composition of growth and profitability changes dramatically as a company scales.

Pre-$10M ARR: At this stage, the Rule of 40 is largely irrelevant. A company growing 80% with a -50% EBITDA margin scores a 30. The metric penalizes it, yet this is likely an excellent, venture-scale business making the correct tradeoff: investing aggressively to capture a market. A far better metric here is the burn multiple, which measures how much cash a company burns to generate each new dollar of ARR.

$10M–$50M ARR: In this growth phase, the Rule of 40 starts to become meaningful. Growth rates naturally decelerate from the triple digits, and the question shifts to whether the business is building operating leverage. Is S&M as a percent of ARR starting to decline? Is the company showing a clear path to profitability? Here, the trajectory of the score is more important than the absolute number. According to the KeyBanc SaaS Survey, the median score in this range is often below 40, but a score of 30-35 with a consistently improving trend is a strong signal.

$50M+ ARR: This is the territory the Rule of 40 was built for. The growth-profitability tradeoff is real and stark. At this scale, consistently hitting 40 is the benchmark for solid performance. According to Jamin Ball's Clouded Judgement newsletter, top-quartile public SaaS companies routinely post scores of 43% or higher, demonstrating that they can sustain both meaningful growth and profitability.

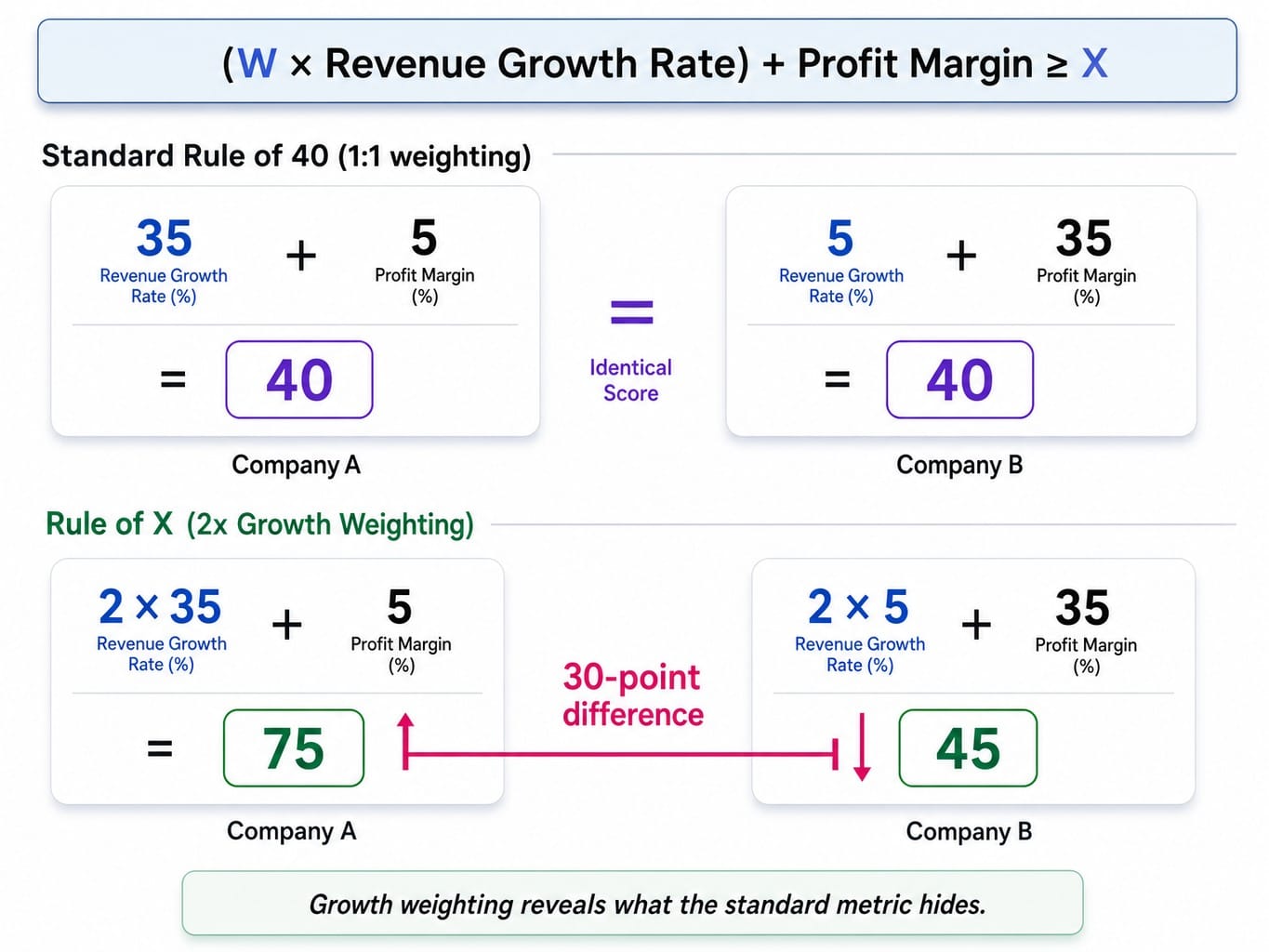

Rule of X: Why Growth Deserves Asymmetric Weighting

The Rule of X is a successor framework to the Rule of 40 that weights revenue growth more heavily than profitability, typically at a 2:1 or 3:1 ratio. It exists to correct the 1:1 flaw, reflecting the empirical reality that public markets value growth-driven performance more than margin-driven performance.

Research from firms like Bessemer Venture Partners has shown that among public SaaS companies, each percentage point of revenue growth contributes roughly 2-3x more to enterprise value than each percentage point of FCF margin. The standard Rule of 40 ignores this. The Rule of X builds it directly into the formula.

The formula can be expressed as:

(W x Revenue Growth Rate) + Profit Margin ≥ X

Where W is the weighting for growth (typically 2 or 3).

Let's re-score our two companies using a 2x growth weighting (a common model in growth equity circles):

- Company A (35% Growth, 5% Margin): (2 x 35) + 5 = 75

- Company B (5% Growth, 35% Margin): (2 x 5) + 35 = 45

Suddenly, the picture is clear. The asymmetric weighting reveals what the standard metric hides: Company A is a far more valuable business. The Rule of X quantifies the compounding power of growth that the Rule of 40 misses.

Of course, there's a catch. This framework can reward unsustainable growth. If your growth is fueled by deeply negative unit economics—a CAC payback period over 18 months or an LTV:CAC ratio below 3:1—then the Rule of X simply amplifies a problem. It should always be used alongside, not instead of, core unit economic metrics. The Rule of 40 is a useful starting point, but the Rule of X is a more accurate reflection of how value is created in SaaS.

How Net Revenue Retention and Cohort Quality Change the Rule of 40 Math

A blended, company-level Rule of 40 score hides the quality of the revenue underneath it.

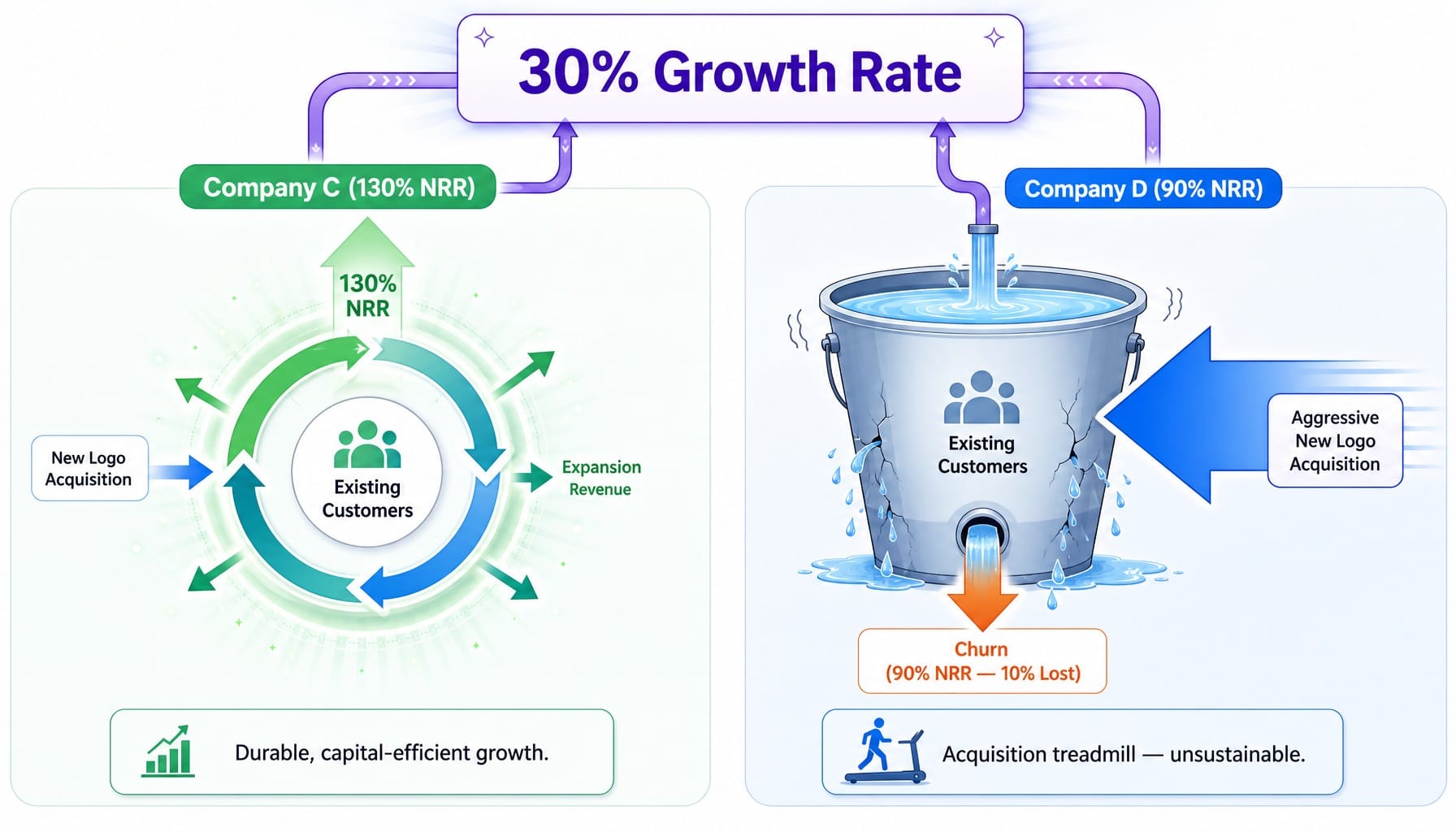

Consider two more companies, both growing at a respectable 30%.

- Company C achieves its growth with 130% Net Revenue Retention (NRR). Its growth is capital-efficient, driven by expansion revenue from happy existing customers.

- Company D achieves its growth with 90% NRR. It's on an acquisition treadmill, constantly needing to acquire more new logos just to replace the revenue churning from its existing customer base.

Their growth rates are identical, but their futures are not. Company C has a durable, profitable growth engine. Company D's model will eventually collapse as its CAC rises and its margins compress.

This is why sophisticated operators and investors decompose the Rule of 40 by cohort. They ask: what is the Rule of 40 contribution from customers acquired in 2023? In 2022? If older cohorts are contributing positive margin while newer ones are still in their CAC payback period, the overall trajectory is healthy. But if older cohorts are churning and only new acquisition is propping up the growth number, the score is a mirage.

Before you report your Rule of 40 to your board, decompose it. Know whether your score is driven by durable expansion from happy customers or an unsustainable new logo acquisition engine. Tools like Maxio, Chargebee, or Mosaic can help segment these metrics, but even a simple spreadsheet can reveal the truth hiding in your blended numbers.

Read more: How to Build SaaS Marketing Attribution That Actually Drives Pipeline (Not Just Dashboards)

When Your Rule of 40 Problem Is Actually a Website Conversion Problem

Improving your Rule of 40 score requires pulling one of two levers: grow faster or improve margin. For most SaaS companies between $5M and $30M ARR, the single most capital-efficient way to improve both sides of the equation at once is by optimizing website conversion.

Higher conversion rates deliver more qualified leads and revenue from the traffic you already have—improving the growth numerator without a proportional increase in sales and marketing spend. This directly lowers your CAC, which in turn improves your margin denominator. It's one of the few levers that positively impacts both parts of the formula.

The problem isn't a lack of insight. Most marketing teams have a long backlog of CRO improvements, landing page experiments, and SEO fixes they know they should ship. The problem is a lack of execution bandwidth. This is a common challenge for teams trying to build a SaaS marketing playbook that compounds results over time.

This is the gap Spike AI is built to close. Every week, Spike AI identifies the highest-impact move you can make across your website, SEO, or ads to increase qualified leads—and then executes it. The compounding effect of these weekly releases directly improves both the growth and margin components of your Rule of 40 score. It's the execution layer that turns conversion insights into shipped improvements, moving the metrics that matter.

See how Spike AI identifies and ships your highest-impact conversion improvements weekly

Conclusion

The SaaS Rule of 40 is a useful screening metric, but it becomes dangerous when treated as a single, definitive number. Its real value lies not in the final score, but in the composition of its two fundamentally different inputs.

Growth compounds; margin on a stagnant base does not. The companies that use this metric well don't just calculate it—they decompose it by cohort, weight growth asymmetrically with frameworks like the Rule of X, and treat it as the beginning of a deeper analysis, not the end.

If your Rule of 40 score looks healthy, ask yourself a harder question: would it survive a cohort-level decomposition? If the answer is no, the score is telling you a story you want to hear, not the one you need to hear.

Frequently Asked Questions

Does the Rule of 40 apply to usage-based SaaS pricing models?

Yes, but with adjustments. For usage-based models like Snowflake's, where contracted ARR is ambiguous, use the annualized revenue from the most recent quarter as your growth input. Be aware that the profitability side is also affected, as gross margins are typically lower due to infrastructure costs scaling with consumption, which can compress the Rule of 40 score.

Can a bootstrapped SaaS company realistically exceed the Rule of 40?

Absolutely. Bootstrapped companies often exceed the Rule of 40 because they are forced to optimize for profitability from day one. A company growing 15% with a 30% EBITDA margin scores a healthy 45. The trade-off is that they rarely achieve the hyper-growth scores that command premium valuation multiples because they aren't making the same aggressive investments in sales and marketing.

What Rule of 40 score justifies a premium SaaS valuation multiple?

According to SaaS Capital and Meritech Capital data, public SaaS companies scoring above 40 trade at a median EV/Revenue multiple roughly 2x higher than those below. However, composition is key. A growth-led 50 (e.g., 35% growth + 15% margin) will command a meaningfully higher multiple than a margin-led 50 (15% growth + 35% margin) because investors price in the compounding effect of growth.

How do AI-native SaaS companies perform on the Rule of 40 differently?

AI-native SaaS companies often exhibit faster revenue growth but have lower gross margins (50-65%) than traditional SaaS (75-85%) due to heavy GPU and inference costs. This compresses the profitability side of the Rule of 40. For these companies, tracking a gross-margin-adjusted Rule of 40 or using contribution margin instead of EBITDA provides a more accurate view of underlying health.

Should you optimize for growth or margin to improve your Rule of 40 score?

It depends on your stage. Below $20M ARR with strong unit economics, optimize for growth, as each point contributes more to enterprise value. Above $50M ARR, margin improvement often becomes the more realistic lever. The worst strategy is cutting costs just to hit 40 while growth stalls—you hit the number but destroy the compounding engine that makes it meaningful.

What are the most common mistakes when calculating the Rule of 40?

Three mistakes dominate. First, mixing input timelines, like using quarterly growth with annual margin. Second, including non-recurring revenue (like services fees) in the growth calculation, which inflates the number. Third, using unadjusted EBITDA that includes one-time charges or large stock-based compensation, which distorts the true profitability of the business.